Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Good Intentions. Real Consequences. A Lesson Massachusetts Has Already Lived.

Whenever housing costs rise, rent control is often presented as a quick fix. The idea sounds reasonable: limit rent increases to protect tenants from sudden spikes. But housing policy is rarely simple—and Massachusetts has already tested rent control, studied it extensively, and reversed course.

As someone who works daily with homeowners, renters, and investors across Greater Boston and MetroWest, I believe it’s important to look beyond slogans and study what actually happens when rent control is implemented—for renters, homeowners, and the overall housing supply.

What Is Rent Control?

Rent control (or rent stabilization) refers to laws that limit how much landlords can charge for rent or how quickly rents can increase. These policies typically apply to existing rental units and may restrict vacancy decontrol, property improvements, or unit conversions.

The goal is to protect tenants from displacement and improve affordability.

The challenge is that housing markets respond to incentives, and decades of research show rent control changes those incentives in predictable—but often harmful—ways.

Massachusetts Has Been Here Before

From 1970 to 1994, cities like Cambridge, Brookline, and Boston had some of the strictest rent control laws in the country. In 1994, a statewide ballot initiative repealed these laws, effectively banning rent control across Massachusetts.

Since then, economists, urban planners, and housing researchers have closely examined what happened during rent control and after its repeal—especially in Cambridge, which had the most aggressive controls.

The findings are remarkably consistent.

What the Data Shows

1️⃣ Rent Control Shrinks Housing Supply

Multiple studies find that rent control reduces the number of rental units over time, as landlords convert rentals into condos, sell to owner‑occupants, or withdraw units from the rental market entirely.

In Cambridge alone, researchers found a significant decline in rental inventory while rent control was in place—and a sharp investment rebound after repeal.

2️⃣ Housing Quality Declines

When rent growth is capped, landlords often cannot justify reinvesting in maintenance or upgrades. Over time, this leads to aging, under‑maintained housing stock—hurting the very tenants the policy aims to protect. After rent control ended in Cambridge, housing investment increased by roughly 20%, and renovation activity surged across neighborhoods.

3️⃣ Rent Control Helps Some Renters—But Hurts Many Others

Research consistently shows rent control benefits current tenants who already occupy controlled units, often at significant discounts. However, it also:

- Raises rents in uncontrolled units

- Makes housing harder to find for new renters

- Reduces mobility, trapping people in units that no longer fit their needs.

In effect, access becomes based on timing—not need.

4️⃣ Homeowners and Neighborhoods Are Affected Too

Rent control doesn’t just affect landlords and tenants. Studies of Cambridge found that rent control lowered surrounding property values and reduced neighborhood investment, affecting homeowners who never owned rental property.

After repeal, Cambridge experienced an estimated $7.8 billion increase in residential property values, much of it from spillover improvements in nearby homes.

Why This Matters Right Now

From my perspective working in Massachusetts real estate, today’s housing challenge isn’t just affordability—it’s supply.

Policies that discourage new construction, renovation, or long‑term rental ownership reduce overall inventory, which eventually pushes rents higher for everyone, especially renters who don’t already have housing.

Rent control may feel like an immediate response, but history suggests it often trades short‑term relief for long‑term scarcity.

A More Effective Question to Ask

Instead of asking “How do we cap rents?”, data suggests we should be asking:

- How do we increase housing supply?

- How do we incentivize development and renovation?

- How do we protect vulnerable renters without shrinking inventory?

Massachusetts’ own experience offers a rare, real‑world case study—and it’s one worth examining carefully.

A Thoughtful Call to Action

Whether you’re a renter, homeowner, or investor, housing policy affects you—directly or indirectly.

Before supporting any proposal:

- Review the data

- Understand Massachusetts’ history

- Consider both intended and unintended consequences

Engage in the conversation informed by evidence, not just urgency. Housing is too important—and too complex—for shortcuts.

Rent control doesn’t eliminate high rents—it often eliminates housing.

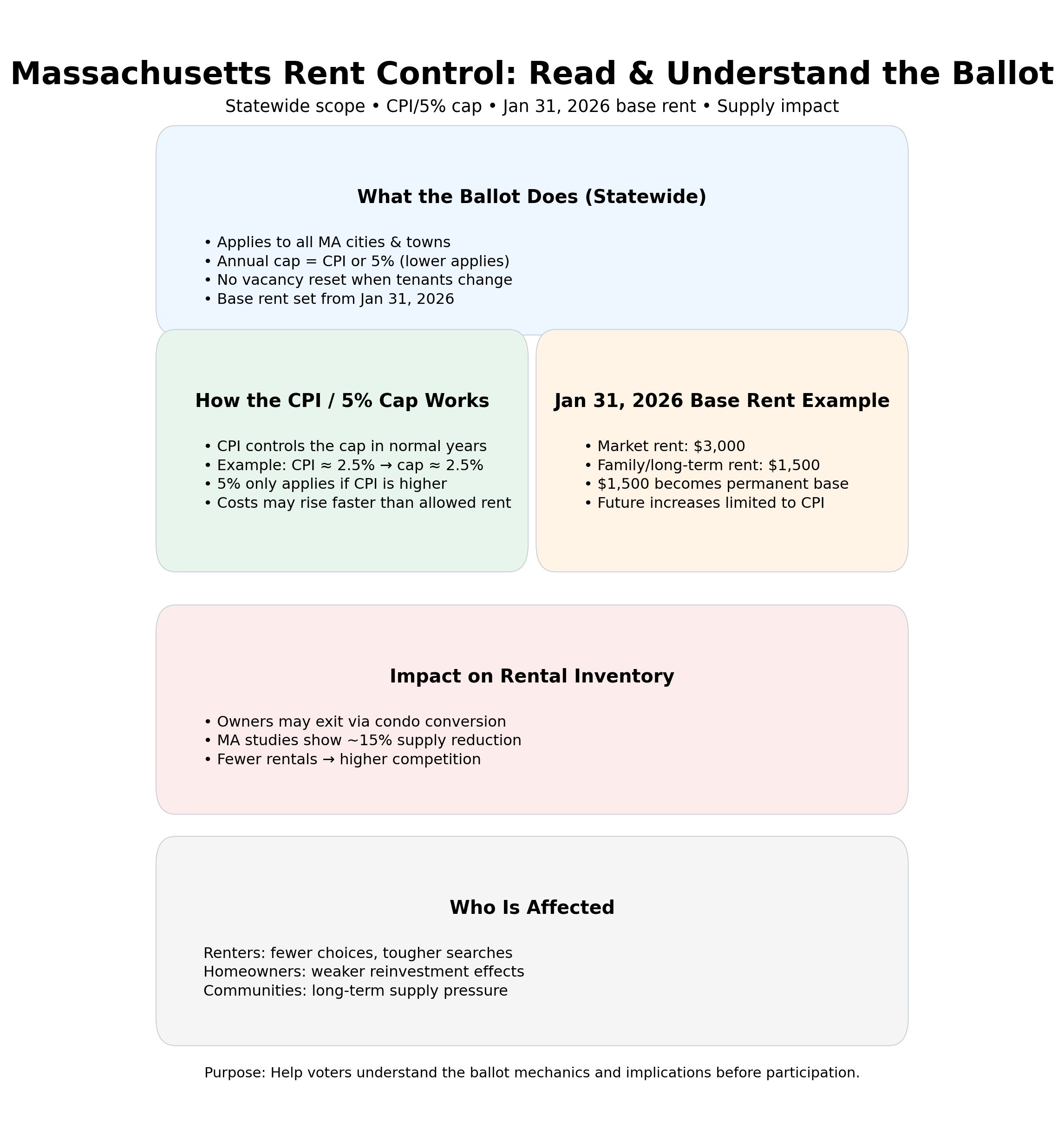

What the Ballot Actually Proposes — And Why the Details Matter

One of the most important parts of this discussion is not just the concept of rent control, but how it would actually be implemented under the current Massachusetts ballot proposal.

According to the published ballot language and independent reporting, the initiative would introduce statewide rent control across all 351 cities and towns in Massachusetts—not just high‑cost urban markets.

Key Terms in the Proposed Ballot Measure

Here’s what the proposal would do:

- Cap annual rent increases at the lower of 5% or CPI

- If inflation (CPI) is 2.5%, then 2.5% becomes the maximum allowed increase

- In higher‑inflation years, increases would still be capped at 5%, not actual cost growth

- This is way below what all the other expenses have gone up for landlords and investors already.

- When inflation is low, CPI—not 5%—sets the ceiling, even if operating costs rise faster than CPI (insurance, taxes, utilities, repairs).

- Apply the cap even when tenants change*

- There is no vacancy decontrol

- Landlords would be prohibited from adjusting rent to market levels after a tenant moves out

- So imagine a scenario where one is renting to a family member at 50% and now they vacate and the new tenant comes- this is sugesting that the landlord cannot adjust the markt rate if this law goes into effect as it currenty is proposed

- Lock rents based on a backward‑looking base date

- The rent in effect on January 31, 2026 would become the permanent “base rent”

- If a unit was vacant on that date, the most recent prior rent would be used

- Apply statewide immediately if passed

- This is not a pilot program or local option

- All covered units across the state would be affected at once

*A Real‑World Illustration: The January 31, 2026 “Base Rent” Problem

The ballot language does something else that’s easy to miss but critical: it locks in rents based on a backward‑looking base date. Here’s how it works:

- The rent in effect on January 31, 2026 becomes the permanent base rent.

- If a unit is vacant, the most recent prior rent is used instead.

Example Scenario: Family or Long‑Term Discounted Rent

Imagine this common, good‑faith situation:

- Market rent for a 2‑bedroom: $3,000/month

- Owner rents to a family member or long‑term tenant at 50% of market: $1,500/month

- That rent is in place on January 31, 2026

What happens next under the proposal?

- $1,500 becomes the permanent base rent

- Annual increases are capped at CPI (~2.5%)

- The rent can never reset to market, even if the tenant leaves

- The discount becomes legislated and permanent

This structure discourages:

- Helping family members

- Rewarding long‑term tenants

- Offering below‑market rents for stability

Instead, it encourages defensive behavior—fewer rentals and tighter screening.

The Unintended Impact of a Retroactive Freeze

From a market perspective, the January 31, 2026 base‑rent rule has implications many people don’t even realize or comprehend.

- Owners who discounted rents for long‑term tenants, family members, or friends would never be able to reset to market

- Units intentionally priced below market to encourage stability would be permanently capped

- Good‑faith pricing decisions made years ago would be locked in indefinitely, regardless of operating cost increases

In practice, this creates a strong incentive for owners to:

- Remove units from the rental market

- Convert to owner‑occupied housing**

- Delay renovations or reinvestment

- Screen tenants more aggressively to reduce turnover risk

The net effect, based on historical precedent, is less rental inventory and fewer choices for renters—especially new renters entering the market.

**Let’s look at one example”

What Happens When Owners Convert Rentals to Condos?

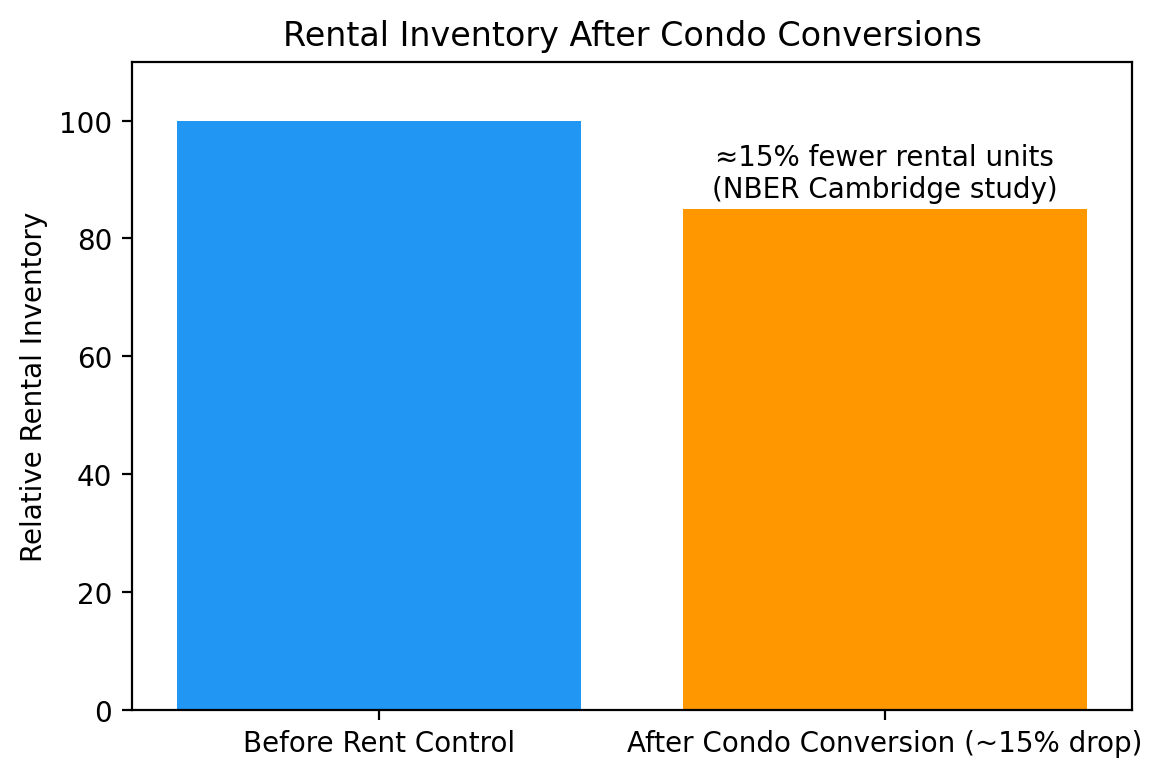

History shows that when rent control caps returns and removes pricing flexibility, many owners exit the rental market altogether—often by converting units to condominiums or owner‑occupancy.

What the Data Shows (Cambridge, MA)

- A major NBER and MIT study found that after rent control expansion in Cambridge, landlords reduced rental housing supply by ~15%, largely through condo conversions and unit withdrawals.

- After rent control was repealed, housing investment rebounded sharply, and neighborhood conditions improved.

Figure: Rental Inventory Decline from Condo Conversions

So what we have is the opposite result: Fewer rentals = more competition for remaining units, which historically leads to higher rents in the uncontrolled portion of the market.

Why This Affects Homeowners Too

Even homeowners who don’t rent out property are not insulated from these effects.

Research from Cambridge shows that restrictive rent policies lower neighborhood investment and suppress surrounding property values, including properties that were never rented any units at all.

Reduced reinvestment and declining inventory don’t just change rental markets—they change the health and growth of entire neighborhoods.

Renters face fewer options, longer searches, and higher competition for available units.

A Massachusetts‑Specific Reality Check

Massachusetts doesn’t need to guess how this plays out—we’ve already lived it. As mentioned above, rent control in the 1970s–1990s:

- Reduced rental supply

- Degraded housing quality

- Benefited a narrow group of occupants while excluding others

- Was eventually repealed by voters statewide

The current proposal is broader, more restrictive, and statewide, with fewer off‑ramps than what existed before 1994.

A Thoughtful Way Forward

Housing affordability is real. Displacement is real. The question is whether price controls that restrict supply are the most effective tool—or whether they repeat past mistakes. Before supporting or opposing any housing policy, it’s worth understanding:

- How incentives change behavior

- How supply responds to restrictions

- Who benefits immediately versus who bears long‑term costs

An Informed Civic Call to Action

Take time to:

- Read the full ballot language

- Understand how the CPI‑or‑5% cap actually works

- Understand the implications of backdating to Jan 1, 2026 and scenarios of below market rate, regardless of the circumstances and what it means to be at the previous baseline of rent

- Consider how fixed base rents and statewide enforcement affect housing availability

As a person who lives and breathes realestate, remember that the housing policy shapes communities for decades—not just election cycles. I’ll leave you with one key thought: When you lock rent prices to yesterday’s market, tomorrow’s housing supply quietly disappears.

The Bigger Picture

Housing affordability is real—but policies that lock prices while shrinking supply often create long‑term shortages that hurt the very people they aim to help.

When it comes time to the ballot, before supporting or opposing any proposal, it’s worth understanding:

- How CPI‑based caps actually limit increases

- Why a fixed 2026 base rent creates permanent distortions

- How inventory losses compound over time