Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Why 2% Mortgage Rates Were an Emergency, Not the Norm

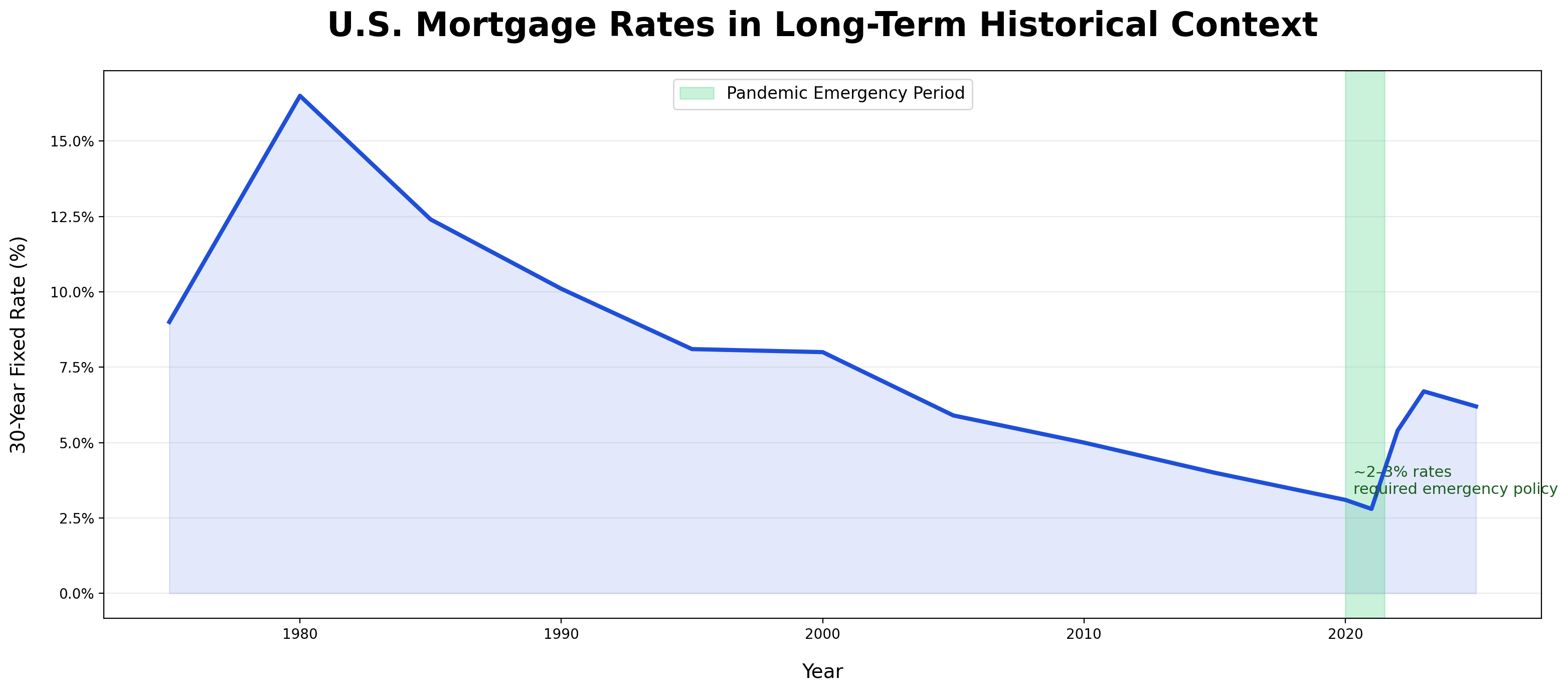

2% mortgage rates didn’t occur during a “normal” housing market. They were the by‑product of a global shutdown, emergency monetary policy, massive government stimulus, and the Federal Reserve buying mortgage bonds at unprecedented levels. Once the economy stabilized, those emergency conditions ended—and so did 2% rates.

Many buyers that I talk to still keep saying “I’ll wait for 2-4% rates again” before buying their home.

My response:

That’s understandable—those rates were historic. But it’s important to know why they happened.

2% mortgage rates only existed because the economy was in crisis: global shutdowns, zero interest rates, trillions in stimulus, and the Fed buying mortgages at an emergency level. Unless we see another event of that magnitude, the conditions that created 2% rates simply don’t exist anymore. Waiting for 2% rates is kind of like waiting for emergency gas prices to come back after a crisis. Those rates weren’t a healthy baseline—they were a response to an economic emergency. Historically, today’s rates are much closer to normal than 2% ever was.

Here is some compiled research done – from varying sources – that is broken into two parts showing why we won’t see the 2–3% unless there is a major economic shock.

- Need to understand first, why mortgage rates went into the low‑2% range

- Then, understand why they are extremely unlikely to return to that range

Part 1: Why Mortgage Rates Got So Low (2020–2021)

Mortgage rates near 2–3% were not “normal market behavior.” They were the result of a once‑in‑a‑generation economic emergency combined with extraordinary government action.

1. A Global Economic Shutdown (COVID‑19)

In March 2020, the global economy experienced an abrupt and severe contraction due to lockdowns, job losses, and widespread uncertainty. Investors rushed out of riskier assets and into safe‑haven assets like U.S. Treasury bonds, pushing bond yields sharply lower. Since mortgage rates closely follow long‑term Treasury yields, mortgage rates fell alongside them.

2. The Federal Reserve Dropped Rates to Near Zero

To prevent a full‑scale depression, the Federal Reserve cut the federal funds rate to 0%–0.25% in March 2020. While the Fed does not set mortgage rates directly, this move anchored short‑term borrowing costs at ultra‑low levels, influencing rates across the entire economy.

3. Massive Quantitative Easing (QE)

The Fed went beyond rate cuts and launched one of the largest quantitative easing (QE) programs in history, purchasing:

- U.S. Treasury bonds

- Mortgage‑Backed Securities (MBS)

By buying hundreds of billions of dollars in MBS, the Fed artificially increased demand, pushing yields down and directly suppressing mortgage rates. At one point, the Fed owned nearly 30% of the MBS market, dramatically distorting pricing.

4. Emergency Fiscal Stimulus

At the same time, the federal government deployed trillions of dollars in stimulus (CARES Act, PPP loans, stimulus checks, eviction/forbearance programs). These measures stabilized consumers and prevented a housing collapse, ensuring mortgage credit continued flowing even during a recession.

5. No Inflation (At First)

Inflation was very low or falling in early 2020 due to suppressed demand. That gave the Fed cover to keep monetary stimulus aggressive without immediate consequences.

✅ Result:

Mortgage rates fell to historic lows—as low as 2.65% for a 30‑year fixed, the lowest ever recorded.

Part 2: Why Mortgage Rates Are Very Unlikely to Return to 2%

Economists overwhelmingly agree: 2% mortgage rates were an anomaly, NOT a baseline.

1. Inflation Has Fundamentally Reset the Floor

Post‑pandemic inflation reached multi‑decade highs, forcing the Fed to aggressively tighten policy. Even as inflation cools, it remains structurally higher than in the pre‑2020 era due to:

- Supply‑chain reshoring

- Wage growth

- Persistent fiscal deficits

- Geopolitical instability

Mortgage rates cannot sustainably fall to 2% unless inflation collapses again—which would almost certainly require another severe recession or crisis.

2. The Fed Is Actively Unwinding QE (Quantitative Tightening)

The Fed is now doing the opposite of what drove rates down:

- Letting MBS roll off its balance sheet

- Reducing liquidity (Quantitative Tightening)

This puts upward pressure on long‑term rates, including mortgages. The Fed has explicitly stated it does not intend to return to aggressive MBS purchases under normal conditions.

3. The “Neutral Rate” Is Higher Now

Economists estimate the economy’s long‑run neutral interest rate is higher than it was pre‑2020, meaning borrowing costs structurally sit higher even in healthy economic conditions.

4. Federal Deficits and Treasury Supply

The U.S. is issuing record amounts of Treasury debt to finance long‑term deficits. Increased supply of bonds requires higher yields to attract buyers—another force keeping mortgage rates elevated.

5. Experts’ Consensus Forecast

Most housing economists expect:

- 5.5%–6.5% to be the new normal range

- Not a return to 2–3% without a major economic shock

Mortgage Bankers Association, Fannie Mae, and NAR economists all describe pandemic‑era rates as non‑repeatable under stable conditions.

The Bottom Line

2% mortgage rates happened because the world was on economic life support.

They required a global shutdown, zero interest rates, massive government stimulus, and the Fed buying mortgages at an unprecedented scale.

Absent another crisis of that magnitude, those conditions are unlikely to return.

Today’s rates feel high only when compared to an unnatural, emergency‑driven moment in history—not when viewed through a long‑term lens.